Venture Capital in Additive Manufacturing

A detailed analysis of the Additive Manufacturing venture capital and startup market

In Additive Manufacturing (AM), rapid innovation and substantial funding were driving forces in the past decade. However, the industry is now navigating in a more challenging environment. The once-thriving ecosystem, characterized by significant investments and flourishing ventures, faces headwinds due to overpromised expectations leading to disappointment and subsequently, the subdued valuation of publicly traded companies in the sector. The top three AM technology startups raised over EUR 1.2 billion in total funding before going public in a SPAC deal. Although their valuation at the time of the IPO in 2021/22 was at EUR 4.6 billion, it has sharply dropped to only EUR 0.5 billion today.

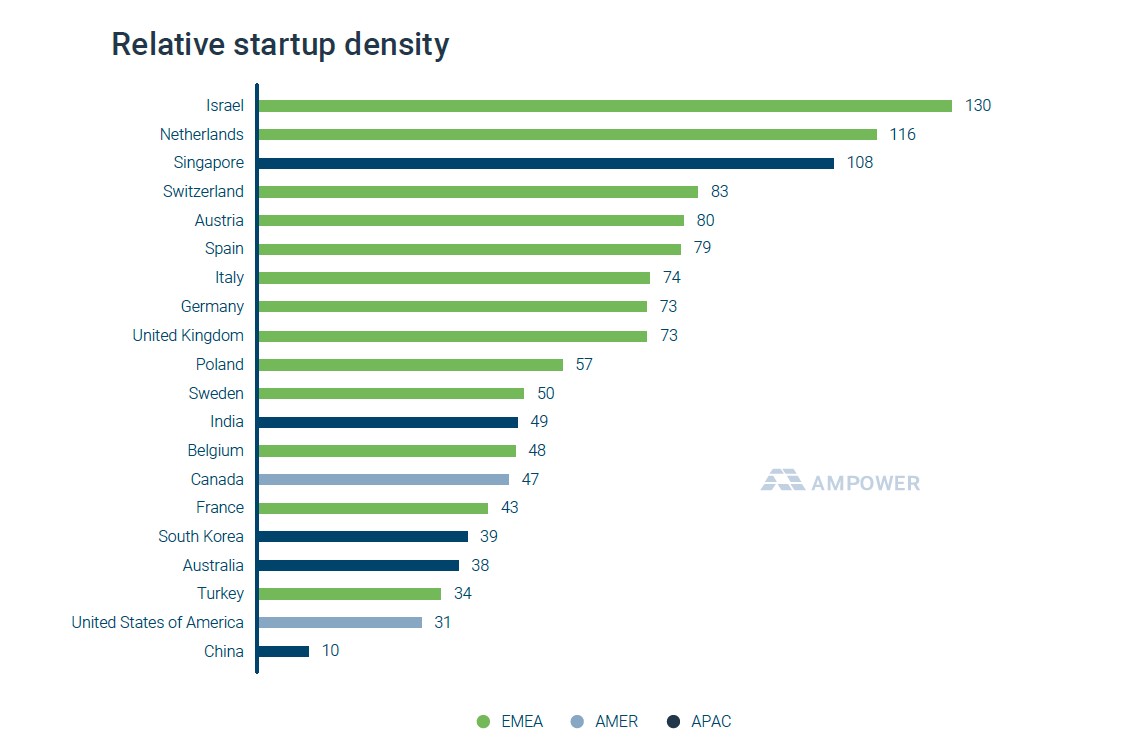

Unsurprisingly, the US boasts the largest number of Additive Manufacturing startups, while Israel and the Netherlands lead in AM startups relative to their countries’ economic power. A surprising second in the Asia Pacific region after China and a newcomer in recent years is India, with over 166 AM startups listed.

While the number of new AM technology startups annually has declined over the past decade, the number of new application-driven AM startups have steadily increased. Additive Manufacturing enables new applications, and while established companies often struggle to fully embrace AM, startups are likely to take the risk associated with a completely AM-driven approach to manufacturing applications.

While startups are currently facing challenges in raising money, investors find attractive opportunities due to lower valuations. However, the number of startups with a truly new value proposition is lower than in the past. Overall, startups with a customer focus and application-centric approaches are poised to have successful funding rounds in the next couple of years.

You need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou need to load content from hCaptcha to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou need to load content from Turnstile to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Hubspot Embedded Content. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from HubSpot. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Hubspot Meetings. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information